If you’re a real estate investor, you’ve likely heard about how cost segregation unlocks massive tax deductions by reclassifying parts of your property into faster-depreciating components. But with the passage of the One Big Beautiful Bill Act (OBBBA), some of the long-standing rules have changed — and the timing of when you do your cost segregation study (or acquire property) could materially affect its tax benefit.

Important Disclaimer: I am not a tax professional. This article is for educational purposes only. Consult your CPA or tax advisor before making any cost segregation or depreciation decisions.

What Is a Cost Segregation Study (Quick Refresher)

A cost segregation study (“cost seg”) is an IRS-approved engineering analysis that reclassifies building components into shorter depreciation schedules (5, 7, or 15 years instead of 27.5 or 39 years).

This can create massive early tax deductions, especially for properties purchased or renovated recently.

Examples of reclassified components:

- Flooring

- Electrical improvements

- Landscaping

- Parking lots

- Millwork and cabinetry

- HVAC distribution

For many of my Arizona investor clients, cost segregation can unlock $30k–$150k+ of first-year depreciation, depending on property type and cost basis.

What Changed Under OBBBA — And Why It Matters for Cost Segregation

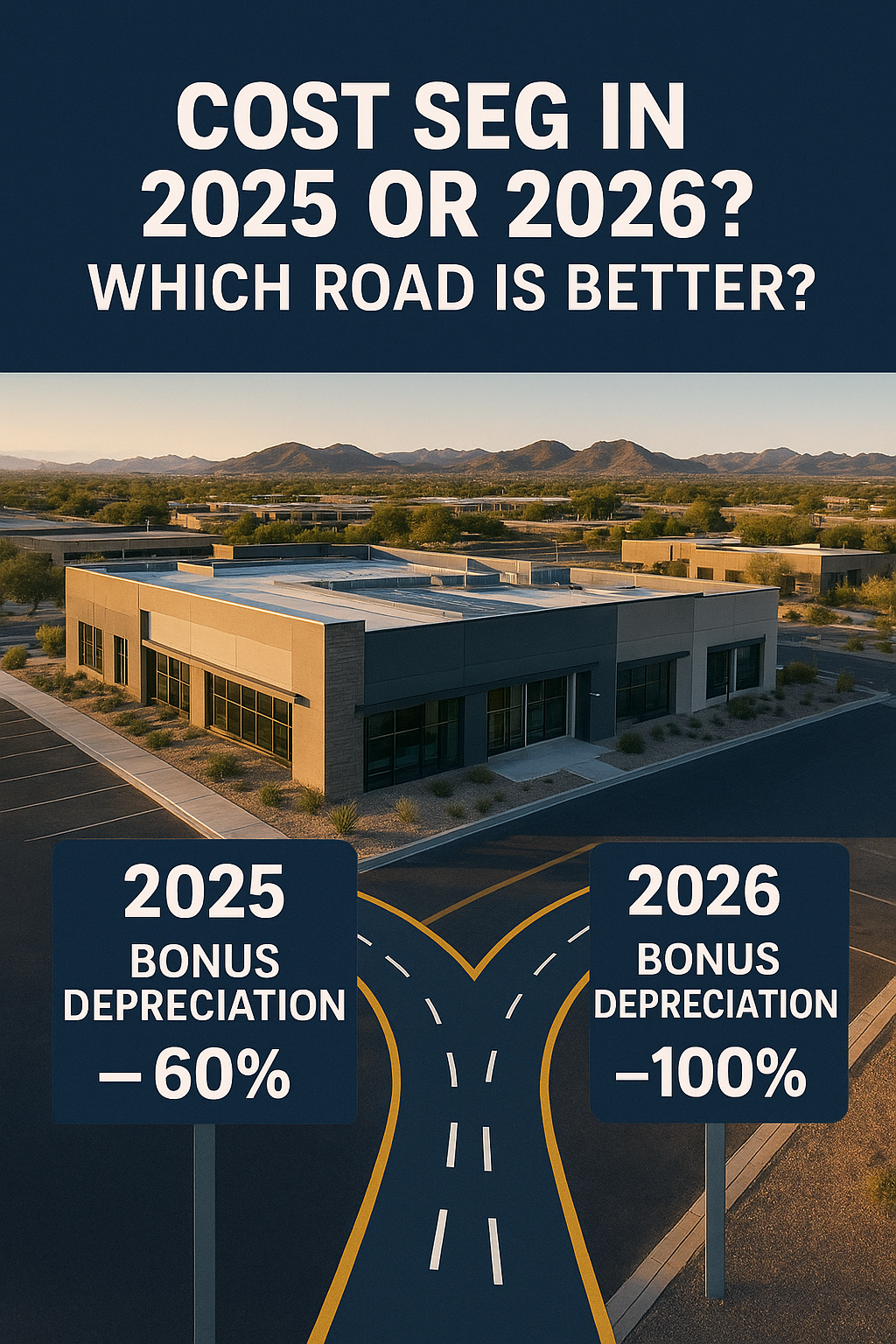

100% Bonus Depreciation Is Back — Permanently

Thanks to OBBBA, 100% bonus depreciation has been reinstated for qualifying assets placed in service after January 19, 2025.That means assets identified through a cost segregation study (like land improvements, fixtures, and other short-lived property) can potentially be fully expensed in the first year.

Qualifying property includes both new and used assets, as long as they meet the acquisition and placed-in-service rules.

Binding Contract Timing Is Critical

Be careful: the law distinguishes when you acquire the property, not just when you place it in service.If you entered a written binding contract before January 20, 2025, even if the property is placed in service after that date, it might not qualify for 100% bonus depreciation.

That makes “contract date” a key planning lever for investors who want to maximize this benefit.

Cost Segregation Is Even More Powerful Now

Because bonus depreciation is fully restored, cost segregation studies become more valuable: you can bump more of your building’s cost into 5-, 7-, or 15-year property categories and expense it immediately.That accelerated deduction improves cash flow dramatically in year one.

This is especially relevant for real estate investors doing value-add renovations or major improvements, where many modern components qualify.

Should You Do a Cost Segregation Study Now (2025) or Wait Until 2026?

Here’s a breakdown of when cost segregation might make sense under the new law — and when it may make more sense to wait.

✅ Arguments For Doing It Now (2025)

- Max Your First-Year Deduction: With 100% bonus depreciation restored, doing a cost segregation study in 2025 can yield a huge write-off immediately.

- Better Cash Flow: That deduction boosts cash flow in your first year of ownership or after a big renovation.

- Planning Certainty: Because the bonus is now permanent, you’re not racing against a phase-out anymore. Planning for future acquisitions gets easier.

- Look-back Opportunities: If you’ve already acquired property but haven’t done a cost segregation study, in some cases you may be able to file a “look-back” IRS adjustment (Form 3115) to catch missed depreciation.

❗ Risks & Reasons to Wait Until 2026 or Later

- Contract Date Risk: If your acquisition contract was signed before January 20, 2025, that could preclude 100% bonus depreciation under OBBBA.

- IRS Guidance Not Final: Treasury and IRS rules around “acquired date” and placed-in-service for OBBBA are still evolving.

- Cost of Study: A cost segregation study typically costs several thousand dollars. If your expected bonus doesn’t justify the cost, the ROI may be weaker.

- Risk of Lower Basis: For long-term hold investors, front-loading depreciation aggressively might reduce basis, which could affect one’s ability to benefit from other tax strategies later (e.g., upon sale).

- State Conformity Risk: Not all states conform to the federal bonus depreciation rules — your state tax liability could end up higher than you expect.

Strategic Recommendations for Real Estate Investors

If you’re leaning into cost segregation under the new OBBBA provisions, here are some tactical tips:

Talk to Your CPA or Cost Seg Engineer Now

Ask specifically about the impact of your acquisition date, your contract timing, and make sure your study aligns with both OBBBA and your long-term hold strategy.Model Your Scenarios

Build cash-flow models for:

- Your property without cost segregation

- With cost segregation + 100% bonus in 2025

- With cost segregation but placing property in service in 2026 or later (if that’s an option)

Be Careful With Timing

If you’re closing a property soon, discuss having your contract or closing structured to optimize OBBBA eligibility.Keep Excellent Documentation

Secure all engineering reports, contracts, purchase documentation, and placed-in-service records. They will matter for IRS review.Coordinate with Exit Plans

If you plan to hold long-term, think through basis reduction, and how accelerated depreciation might affect your eventual tax situation — including sale, 1031 exchanges, or entity strategies.

Final Thoughts

Cost segregation has never been more compelling. With the permanent reinstatement of 100% bonus depreciation under the One Big Beautiful Bill Act, now (2025) is a particularly powerful moment to consider a study — provided your timing, structure, and documentation are clean.

But it’s not a one-size-fits-all. That “front-load” benefit comes with trade-offs, especially for investors focused on long-term basis, exit strategy, or properties acquired under older contracts.

Talk to your advisor. Run the numbers. The right cost segregation move now could unlock serious cash flow — but only if done smartly.

Check out our full guide: Arizona Real Estate Investor’s Guide – From First Deal to Scalable Portfolio

DTD Realty — Do The Deal.

Driven. Trusted. Dependable.

📞 602.702.3601

🌐 https://www.dtdrealty.com

📩 [email protected]